The Cotswolds has been told to build 1,036 homes a year. That number comes from a formula. It takes the district's existing housing stock, applies a baseline growth rate of 0.8%, then adjusts upwards based on the ratio of house prices to local earnings. The Cotswolds is expensive. So the formula generates a big number.

It doesn't ask how much land is actually available for development. It doesn't check whether the water supply can cope, or the roads, or where the children are supposed to go to school. Eighty per cent of the district is protected National Landscape where large-scale development should only happen in exceptional circumstances. The formula doesn't account for any of this.

The adopted Local Plan set a requirement of 420 homes per year. The new figure is a 147% increase, imposed overnight by a change to national planning policy.

Until December 2024, councils in this position had an option. The National Planning Policy Framework included a clause allowing local authorities to argue that exceptional circumstances justified a lower housing target. Protected landscapes, national parks, infrastructure constraints. The government consulted on removing that clause. Most respondents disagreed. The Local Government Association warned it would strip councils of local flexibility. The government removed it regardless, stating that it is "essential that we have a planning system geared toward meeting housing need in full."

The result is a formula that will force development into areas that cannot absorb it, and no legitimate route to push back.

How the formula actually works.

The standard method has two steps. Step one takes 0.8% of existing housing stock, as recorded in the government's own dwelling stock estimates (MHCLG Table 125). As at March 2023, the most recent figure available when the December 2024 target was set, Cotswold District had 46,213 dwellings. That gives a baseline of 370 homes per year.

Step two applies an affordability adjustment. The formula uses the ratio of median house prices to median workplace-based earnings, averaged over five years. Where that ratio exceeds 5, an uplift is applied that rises steeply with the gap: a ratio of 10 nearly doubles the baseline, a ratio of 15 almost triples it. The Cotswolds five-year average is high enough to push the baseline of 370 up to 1,036.

That is the entire basis for a number that determines where tens of thousands of homes will be built, which fields get developed, which villages change beyond recognition, and which councils lose the ability to refuse.

The Planning Officers Society has called it a "huge mistake" and a "proxy, unrelated to an area's housing need." Understanding why requires looking at what the formula actually measures and what it chooses to ignore.

Get the dispatch.

Long-form, data-first, independent. Housing, planning and infrastructure reporting delivered free to your inbox.

It penalises areas for being protected. House prices in the Cotswolds are high because it is a National Landscape with strict controls on development. People pay a premium to live somewhere beautiful and unspoilt. The formula reads those high prices as unmet demand and converts them into a higher target. But building 1,036 homes a year won't make the Cotswolds affordable. The demand isn't coming from local workers priced out of their own area. It's coming from equity-rich buyers relocating from London and the South East, retirees downsizing, second-home purchasers. These buyers will continue to outbid local workers regardless of how many homes get built. Savills data from 2025 shows that almost half of Cotswolds buyers relocated from London. The formula treats this as local housing need.

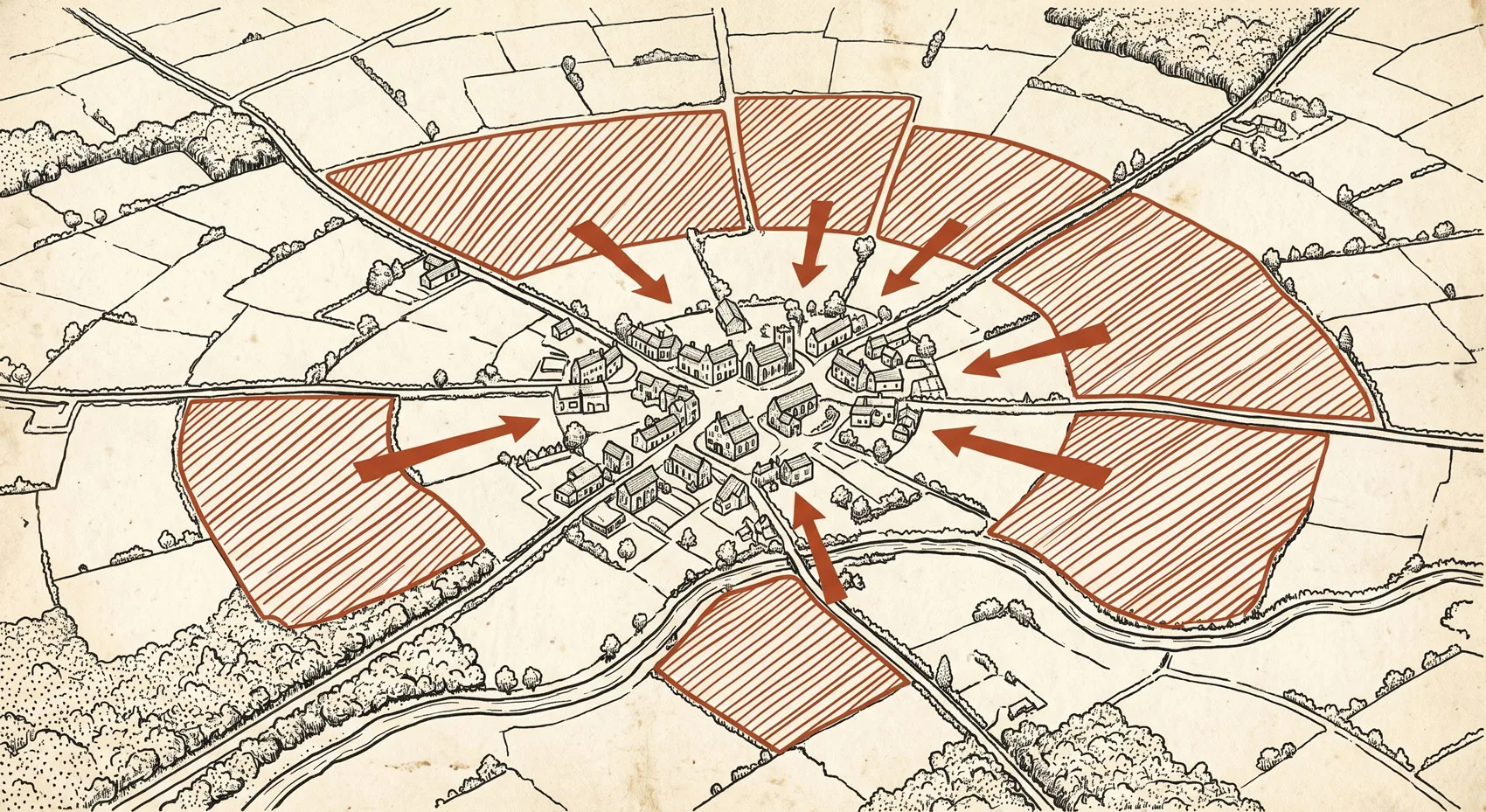

Some of the people the formula claims to help are local residents priced out of communities where they grew up. That is a real problem. But this formula doesn't solve it. What gets built is developer-led estates on the edges or in market towns, high-density designs that bear no relationship to the places they sit in, priced for equity-rich buyers relocating from elsewhere. In Cotswold District, where the new formula more than doubled the annual housing target and 84% of the district is constrained by protected landscape and flood risk, growth is being funnelled onto the 16% that is left. One hamlet faces proposed growth of 1,271%, a change the Cotswold Planning Hub describes simply as "from hamlet to town." Preston faces 268% growth. Kemble faces 180%, despite a neighbourhood plan backed by 95.6% of residents. Rural social housing waiting lists grew 31% between 2019 and 2022 while urban lists grew just 3% (National Housing Federation). Just 2,831 social homes were built across all of rural England last year (CPRE, 2025). The formula generates volume. It does not generate the right homes, in the right places, for the people who actually need them.

There's a further problem nobody in government seems willing to address. If building more homes doesn't reduce prices (and in an area like the Cotswolds, it won't), the affordability ratio stays high. Which means the formula keeps generating the same inflated target. Year after year after year. The circularity is baked in. ONS data shows the Cotswolds affordability ratio has actually improved, falling from a peak of 15.70 in 2021 to 13.43 in 2025, the lowest since 2018. But the formula uses a five-year average, which means the COVID-era price spike remains embedded in the calculation until it drops out of the averaging window. Affordability improves. The target doesn't move. The areas more protected will only increase further also.

It uses the wrong earnings data. The standard method measures workplace-based earnings: what people who work in the Cotswolds earn. But many of the people buying homes there don't work in the district. They commute to Swindon, Cheltenham, Oxford, London, Bristol. Or they're retired. The ONS itself notes that 60% of mortgages are based on joint income, yet the formula uses individual earnings. It excludes the self-employed entirely. And its own bulletin acknowledges that areas with high proportions of commuters show the largest gap between what workers earn and what residents earn (ONS, Housing Affordability in England and Wales: 2025). The actual household incomes of the people purchasing property are significantly higher than the local workplace median. So the affordability ratio overstates the gap between earnings and prices, and the target is inflated beyond anything a more honest measure would produce.

The formula also ignores demographics almost entirely. ONS provisional data for mid-2025 recorded 653,000 births against 651,000 deaths across the UK: natural population growth of just 2,000 people. Net international migration of 204,000 accounted for over 99% of population growth in the year ending June 2025 (ONS, "Provisional population estimate for the UK: mid-2025," 27 November 2025). Meanwhile, the over-55s hold approximately 75% of all housing equity, and much of the existing family housing stock is stuck. Older owners who might move on have nowhere sensible to move to, punitive stamp duty if they try, and a shortage of genuinely desirable retirement housing. Savills itself has argued that unlocking this movement would do more for the market than new supply alone. A formula that generates housing targets without reference to any of this is not measuring need. It is measuring something else entirely.

The land isn't there. Even setting aside whether the target makes sense in principle, Cotswold District Council's own assessment finds only 16% of the district "relatively free of primary constraints." Their preferred development scenario, the most ambitious option they tested, could only identify capacity for roughly 14,660 homes. The target is 18,650. That's 79%. There is not enough suitable land.

The formula guarantees its own failure. If the council can't hit 1,036 homes a year (and it can't), the housing land supply stays below five years. With only 1.8 years of supply, local housing policies are deemed out of date, and the "tilted balance" kicks in: a presumption in favour of granting planning permission. Developers know this. They are already filing applications on sites that would have been refused 18 months ago. Catesby Estates has submitted an application for 170 homes on agricultural land at Mickleton, next to the National Landscape boundary, explicitly referencing the council's inability to demonstrate a five-year supply. Over 2,030 sites were submitted through the council's Call for Sites in late 2025 (source: CDC consultation summary, March 2026). That's the scale of speculative interest now targeting the district.

The formula doesn't deliver the homes communities need. It delivers a policy vacuum that developers exploit.

What the government changed.

In December 2024, the revised NPPF made three changes that closed off every route councils had to manage this situation.

The standard method was made explicitly mandatory. The December 2023 version, published under the previous Conservative government, had described it as an "advisory starting point." Councils had discretion. That language was removed.

The exceptional circumstances clause was stripped out. Previously, councils could argue that the unique constraints of their area justified departing from the standard method figure. For a district like the Cotswolds, where 80% of the land is nationally protected, this was the obvious route. The government removed it deliberately, after consultation, knowing full well what it would mean for constrained areas.

The affordability adjustment was changed so that expensive areas receive higher targets than before. Rural districts with high house prices got hit hardest. Damian Hinds, MP for East Hampshire, told Parliament on 17 December 2025 that the 58 mainly or largely rural local authorities faced an average uplift of 70%, compared to 50% nationally (Hansard, Housing Development: Cumulative Impacts debate).

At the same time, the Planning and Infrastructure Act 2025 (Royal Assent 18 December 2025) has restricted judicial review of planning decisions. The paper permission stage for challenges has been removed. Where a judge deems a case "totally without merit" at oral hearing, the right to appeal to the Court of Appeal goes too.

Accept the target, lose your plan, or lose control entirely. Those are the options.— The Editor · Ground Level, April 2026

The council that fought back.

East Hampshire District Council is the only authority that has publicly challenged the standard method since the December 2024 changes. Their situation mirrors the Cotswolds. Fifty-seven per cent of the district sits inside the South Downs National Park, where development is restricted. The standard method target nearly doubled to 1,142 homes per year. The land outside the park has to absorb almost all of it.

In mid-2024, the council instructed Paul Brown KC of Landmark Chambers to advise on whether they could depart from the standard method. His initial advice was blunt: any Local Plan that failed to meet the government's target would likely be found unsound. The consequences, he said, would be "catastrophic."

Then the December 2024 NPPF came with updated Planning Practice Guidance. Brown KC looked again. His second opinion, delivered in early 2025, was more favourable. He concluded that the new guidance supports "disaggregating" the housing need: separating the need arising inside the national park from the need outside it, on a pro-rata basis using housing stock proportions. He endorsed a reduced target of 828 homes per year and described this approach as "relatively easy to defend" at examination.

The council called it "not a get out of jail card." They were right to be cautious. In December 2025, Portsmouth, Gosport, and Havant all wrote to East Hampshire asking it to absorb part of their housing shortfall. They can't find the sites to meet their own targets. The council leader responded that East Hampshire is "not a development dumping ground," but conceded they have a legal duty to consider the requests.

The next Local Plan consultation is due this summer, with a Planning Inspector examination in 2027. That examination will be the first real test of whether the disaggregation argument holds up. It matters for the Cotswolds because the same logic applies. If anything, the case is stronger: eighty per cent National Landscape coverage compared to East Hampshire's fifty-seven per cent. Cotswold District Council hasn't pursued this route. Whether they will may depend on what happens in Hampshire first.

East Hampshire is also being carved up by local government reorganisation. The government confirmed in March 2026 that Hampshire will form four new unitary authorities. East Hampshire gets split between two of them. Nobody has explained what that means for the Local Plan they're trying to get through examination.

The reorganisation trap.

This is the part that could end up mattering more than any of the above, and almost nobody is paying attention to it.

Gloucestershire is being reorganised. The six district councils and the county council will be replaced by one or two new unitary authorities. Three options were consulted on. The consultation closed on 26 March 2026. The government's decision is expected in June or July. Elections to the new authority in May 2027. Operational from April 2028.

Before getting to what this means, look at the housing position across the county. Every district's published five-year housing land supply position. The required minimum is five years.

Cotswold District: target 1,036 per year. Supply: 1.8 years (CDC Housing Land Supply Report, June 2025).

Forest of Dean: target 600. Supply: 1.81 to 1.93 years (appeal decision, August 2025).

Cheltenham Borough: target 824. Supply: 2.52 years (CBC briefing note, December 2024).

Gloucester City: target 700. Supply: 3.1 years (GCC Five-Year Housing Land Supply Statement, October 2025).

Stroud District: target 820. Supply: 3.24 years (confirmed at appeal, November 2025). Plan found unsound by inspectors in April 2025.

Tewkesbury Borough: target 614. Supply: 3.65 years against the previous lower target of 554 (TBC Five Year Housing Land Supply Statement, November 2024). No updated calculation against the current higher target has been published. Despite this, Tewkesbury has been the only authority in the South West to historically deliver homes at a rate exceeding its new standard method requirement (LandTech, 2025), according to MHCLG data.

Every single one is failing. Not one Gloucestershire district can demonstrate a five-year housing land supply. This is not a failure of local delivery. It is the direct and predictable consequence of a formula that sets targets without reference to whether they are achievable. The combined target across the county is approximately 4,594 homes per year. Combined delivery is around 3,147. A shortfall of nearly 1,450 homes every year.

Now merge them.

Under a single unitary authority, that combined shortfall becomes one council's problem. The district boundaries that currently keep Cheltenham's unmet need separate from the Cotswolds disappear. Cheltenham delivers 28% of its target and has almost no land left. The Cotswolds has open countryside but is 80% protected landscape. Where does the pressure go?

Cheltenham, Gloucester, and Tewkesbury are already working on a joint Strategic and Local Plan that needs to find sites for over 43,000 homes. Roughly 25,000 still need to be allocated. Their options include Green Belt release and up to three new towns. Under reorganisation, this planning area and the Cotswold planning area merge. Nobody has confirmed what happens to the separate plans.

Housing Minister Matthew Pennycook has been asked directly in a parliamentary written answer (May 2025) what happens to housing targets after merger. His response: "the implications of local government reorganisation, including the impact of reorganisation on local housing targets, will be considered in light of the specific circumstances of any given area." That is the only guidance available. No methodology. No formula. No commitment.

Kent County Council produced a detailed analysis of the housing delivery implications for each of its proposed unitary models before submitting them to government. Gloucestershire has not done this. Nobody has assessed what merging these six failing authorities actually means for where homes get built.

The government has been explicit about what it wants from reorganisation. The GOV.UK consultation document states it will "speed up house building." Damian Hinds MP warned in Parliament that some see reorganisation as a way to solve housing problems. He fears the opposite: "the creation of these large authorities might deepen or even embed these issues, with more housing being moved into countryside that will then be lost forever."

Cotswold District Council's own committee papers (July 2025) contain a line that deserves more attention. They warn that if reorganisation requires restarting the Local Plan process, it could result in a five to seven year delay. Five to seven years without an up-to-date plan. Five to seven years of the tilted balance. Five to seven years of developers filing for whatever they want, wherever they want.

Meanwhile, Gloucester City Council applied for emergency financial support of up to £17.5 million in December 2025 to avoid bankruptcy. The government approved £15.5 million in February 2026. This is a council that may be merging with the Cotswolds to form a new planning authority responsible for delivering thousands of homes across a combined area.

What this means.

None of this is to say local people don't need homes. They do. Young adults across rural England are being priced out of the communities they grew up in. Over a million households sit on social housing waiting lists. That is real and it matters.

The question is what kind of shortage this actually is. Ian Mulheirn's analysis for the UK Collaborative Centre for Housing Evidence found that since 1996, English housing stock has grown faster than the number of households, with the surplus of dwellings over households rising from 660,000 to over 1.1 million. There are 303,143 long-term empty homes in England as of October 2025 (Action on Empty Homes). Developers have secured planning permission for more than 1.4 million homes since 2007 that remain unbuilt (IPPR, 2025). Around 10 million households live in under-occupied homes, because the market doesn't flow. Bank of England Staff Working Paper No. 837 found that falling real interest rates since 1985, not a shortage of homes, fully account for the rise in UK house prices relative to earnings. The implication is not that the Bank should hike rates to bring prices down. It is that house prices have been set by the cost of capital, not by the physical supply of homes. Building more addresses the wrong variable.

England does not have a generalised shortage of housing. It has a shortage of the right homes, in the right places, at prices local people can afford. Those are different problems with different solutions. Building 300,000 market homes a year addresses the first diagnosis. It does almost nothing for the second.

Defenders of the formula will point out that developments include affordable housing quotas, typically 30 to 40%. In practice these are routinely negotiated down through viability assessments. Even when delivered in full, the "affordable" label is a blended figure. A 40% affordable quota might mean 10% social rent, 15% affordable rent capped at 80% of market rate, and 15% shared ownership. Only the first category is genuinely affordable on median local earnings. The rest still requires a mortgage and prices that move with the market.

This is where the formula interlocks with the financial system. New housing creates new mortgageable collateral. Government schemes then layer further credit on top. Help to Buy Equity Loan, which ran from 2013 until 2023, let buyers stack a taxpayer equity loan on top of their mortgage on top of their deposit, three layers of financing against one house. The IMF, Mervyn King at the Bank of England, and recent research from the IFS and academic economists have all found that Help to Buy inflated prices rather than making homes affordable, and benefited developers more than first-time buyers.

The equity loan was retired. But in July 2025 the Mortgage Guarantee Scheme, which backstops 95% loan-to-value mortgages with taxpayer money, was made permanent for the first time, rebranded as Freedom to Buy. Shared ownership works by similar logic: the occupant takes a mortgage on their share, the housing association takes on debt for the rest, and rent is charged on top. Every one of these layers is a financial claim on the same physical house. The political branding changes but the underlying mechanism does not.

The deeper issue is who ends up owning all of this. Build-at-scale delivery concentrates stock in the hands of volume housebuilders, institutional investors, and pension funds, with eligibility and allocation rules set centrally. Distributed ownership, whether owner-occupation, small landlords, or locally built council housing, spreads decisions about where and how people live across millions of people. Centralised delivery funnelled through corporations, layered with government-backed credit, and allocated by rule does the opposite. Building more, under the current framework, isn't neutral. It's choosing one of those futures over the other.

So why is the government pursuing a strategy the evidence doesn't support?

Because the strategy serves the financial system. The UK has £1.7 trillion in outstanding mortgage debt across 12.4 million loans, up from £1.46 trillion pre-pandemic in 2020, nearly a quarter of a trillion pounds added in five years. Gross mortgage lending is now running at around £280 billion a year, with £80.4 billion advanced in the third quarter of 2025 alone, the largest quarterly jump since 2020. Residential property transactions generated £10.4 billion in stamp duty in 2024-25. Construction contributes roughly 6% of GDP, which the OBR can model directly into its forecasts. Building 300,000 new homes a year, at typical prices and loan-to-value ratios, adds around £80 billion of fresh mortgage collateral to this system every year.

Institutional capital is moving in at scale. Build-to-Rent investment reached £5.3 billion in 2025 and is forecast to exceed £5.7 billion in 2026. Legal & General has committed £1.5 billion to affordable housing. AustralianSuper, Nest, and others pledged a further £3 billion in October 2025. The UK's local government pension schemes hold £400 billion in assets, projected to reach £1 trillion by 2040, with a coordinated push to redirect a larger share into housing. In December 2025 the government launched a National Housing Bank with a mandate to deploy £16 billion in debt, equity and guarantees, and to unlock a further £50 billion of private institutional capital on top. JLL forecasts that global investment into "living" real estate could reach 30% of all real estate investment by 2030.

One company illustrates the scale. Blackstone, through Sage Homes, is now the largest provider of newly built affordable homes in England and has been for four consecutive years, with a portfolio of 20,000 UK homes and £3.7 billion committed. Its market-rent arm Leaf Living separately agreed a £1.4 billion deal with housebuilder Vistry to buy 4,500 homes off the production line. Last year Blackstone sold 3,000 shared ownership homes to the UK's largest pension fund for £405 million, a pure financialisation transaction in which retirement capital recycles into housing infrastructure.

The direction of travel elsewhere is the opposite. In January 2026, Donald Trump signed an executive order titled "Stopping Wall Street from Competing with Main Street Homebuyers," directing federal agencies to block institutional investor purchases of single-family homes and authorising antitrust review of their market practices. "People live in homes, not corporations," the order read. At the same time, the UK government launched the National Housing Bank explicitly to channel more institutional capital into housing, and secured pension fund commitments of £3 billion in a single month. The two countries looked at the same model and drew opposite conclusions.

None of this requires the homes to be affordable. None of it requires them to go to local people. The formula doesn't measure housing need. It measures how much development the financial system requires.

The real problem in places like the Cotswolds is not that too few homes exist. It is that the homes which do exist are being purchased by people with equity and incomes that bear no relationship to the local economy. That is a demand-side problem, not a supply-side problem. The formula treats it as supply-side and prescribes mass building. That is the gap between what the government says this policy is for and what it actually does.

Nobody is against homes being built for local people. But those homes need to be the right homes in the right places. Small-scale, well-designed, and genuinely affordable on local wages. Not 150-house estates on greenfield sites at the edge of market towns, built to a density and design that belongs in a suburb, priced for London money, and approved because a formula made it impossible to say no.

A hundred and eighty-nine councils across England cannot demonstrate a five-year housing land supply (Urbanist Architecture, January 2025). The standard method was supposed to simplify and depoliticise housing numbers. What it has actually done is strip out local knowledge, ignore physical constraints, and create a system where councils either accept targets they cannot deliver or lose control of development altogether.

The countryside doesn't get destroyed because nobody cares about it. It gets destroyed because a formula treats it as a delivery mechanism for a financial system that needs perpetual growth.— The Editor · Ground Level, April 2026

The government removed the right to argue otherwise. It has made the formula binding, closed the exceptional circumstances route, and is simultaneously merging the councils responsible for planning into larger entities with combined shortfalls. It has given no clear answer on what happens to targets after merger, carried out no impact analysis for Gloucestershire, and is restricting routes to legal challenge through the Planning and Infrastructure Act.

The next piece will look at infrastructure: water supply, sewage treatment capacity, roads, schools. The numbers the government is demanding assume the infrastructure exists to support them. The Infrastructure Delivery Plans being prepared across the country are likely about to show that it doesn't.

A later piece in this series will examine the financial system behind the 300,000 target in detail. Who benefits, how the money flows, and why the formula is designed the way it is.